Principles of Accountancy is the backbone of every financial system, helping businesses and individuals track their financial transactions effectively. Understanding the principles of accountancy is essential for students, entrepreneurs, and finance professionals to make informed financial decisions. This guide will cover the key objectives, functions, branches, merits, demerits, concepts, and conventions of accountancy, along with its success in India.

Principles of Accountancy Objectives:

The primary objectives of accountancy are:

- Recording Transactions: Systematic recording of financial transactions in books of accounts.

- Classifying Transactions: Organizing recorded transactions into categories for clarity and easy retrieval.

- Summarizing Financial Data: Preparing financial statements such as profit and loss accounts and balance sheets.

- Analyzing Financial Performance: Assessing business profitability and financial position.

- Providing Financial Information: Helping stakeholders make informed financial decisions.

- Compliance and Legal Requirements: Ensuring adherence to tax laws, accounting standards, and financial regulations.

- Budgeting and Forecasting: Aiding in financial planning and resource allocation.

Principles of Accountancy Functions:

Accounting plays a crucial role in financial management. Its key functions include:

- Recording Financial Transactions: Ensuring all monetary transactions are documented systematically.

- Financial Analysis and Interpretation: Providing insights into a company’s financial health.

- Compliance and Auditing: Ensuring financial accuracy and adherence to legal frameworks.

- Cost Management: Helping businesses optimize costs and enhance profitability.

- Decision Making: Offering financial data to guide strategic business decisions.

- Tax Planning and Compliance: Assisting in tax calculations and ensuring regulatory compliance.

Branches of Accounting

Accountancy is broadly classified into various branches, each serving specific purposes:

- Financial Accounting: Deals with recording, summarizing, and reporting financial transactions.

- Managerial Accounting: Focuses on internal financial management and decision-making.

- Cost Accounting: Analyzes production costs and helps in cost control.

- Tax Accounting: Involves tax planning, filing tax returns, and ensuring compliance with tax laws.

- Auditing: Examines financial statements for accuracy and compliance.

- Forensic Accounting: Investigates fraud, financial irregularities, and legal disputes.

- Government Accounting: Manages public funds and ensures accountability in government finances.

Merits of Accountancy

Accounting offers numerous advantages to businesses and individuals:

- Systematic Financial Recording: Ensures an organized approach to managing financial data.

- Better Decision-Making: Provides reliable financial information for business strategies.

- Compliance and Transparency: Helps in legal and regulatory compliance.

- Financial Control: Aids in monitoring expenses and income for effective budgeting.

- Facilitates Loans and Investments: Well-maintained financial records enhance creditworthiness.

- Prevention of Fraud: Helps detect financial discrepancies and frauds.

Demerits of Accountancy

Despite its advantages, accounting has some limitations:

- Does Not Reflect Non-Monetary Factors: Accounting only records financial data, ignoring qualitative factors like employee efficiency and brand value.

- Historical in Nature: Financial statements reflect past transactions, making future predictions challenging.

- Possible Manipulation: Misrepresentation of financial data can mislead stakeholders.

- Complexity in Large Organizations: Managing financial records in big corporations can be complex and time-consuming.

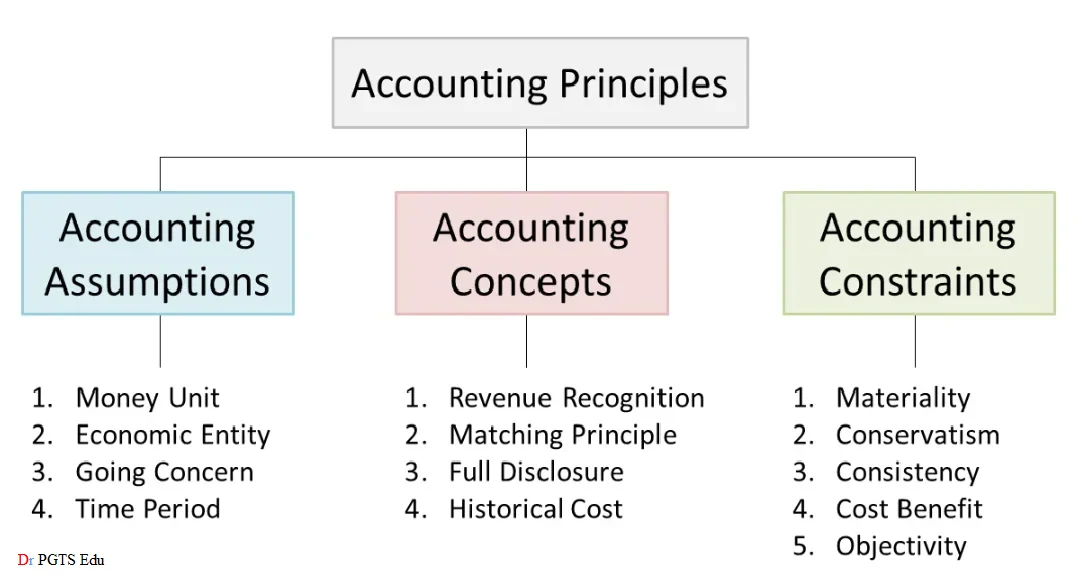

Concepts of Accounting

The fundamental concepts guiding accounting include:

- Business Entity Concept: Business and owner are treated as separate entities.

- Money Measurement Concept: Only monetary transactions are recorded.

- Going Concern Concept: Assumes a business will continue operations indefinitely.

- Accrual Concept: Revenue and expenses are recorded when they occur, not when cash is received or paid.

- Dual Aspect Concept: Every transaction affects two accounts (debit and credit).

- Matching Concept: Revenues and related expenses are recorded in the same accounting period.

Conventions of Accounting

Accounting conventions ensure consistency and reliability. These include:

- Consistency Convention: Accounting methods should remain uniform over time.

- Conservatism Convention: Recording anticipated losses but ignoring unrealized gains.

- Materiality Convention: Significant financial information should be disclosed.

- Full Disclosure Convention: All essential financial information must be shared with stakeholders.

Success of Accounting in India

India has seen tremendous progress in the field of accountancy due to economic growth and evolving financial regulations. Some key aspects of its success include:

- Adoption of International Accounting Standards: India follows the Indian Accounting Standards (Ind AS), aligned with IFRS.

- Growth of Chartered Accountancy Profession: The Institute of Chartered Accountants of India (ICAI) ensures high standards in accounting education and practice.

- Increased Financial Transparency: Government initiatives like GST and digital transactions have improved accounting efficiency.

- Boom in Financial Technology: Digital accounting software and cloud-based financial tools have enhanced accuracy and accessibility.

- Stronger Compliance Framework: Stringent financial regulations and auditing standards ensure corporate accountability.

Understanding the principles of accountancy is crucial for managing finances effectively, whether in business or personal life. With well-defined objectives, functions, concepts, and conventions, accounting helps maintain financial stability and transparency. In India, the accounting profession continues to grow, supported by technological advancements and regulatory improvements. By mastering these principles, individuals and businesses can make informed financial decisions and achieve long-term success.

Read also: Terms a accounting principles