What is a Not-for-Profit Organisation?

A Not-for-Profit Organisation (NPO) is an entity that operates for a purpose other than making a profit. Instead of distributing earnings to owners or shareholders, an NPO reinvests any surplus funds into its mission, which could include social, educational, charitable, religious, or cultural objectives.

Key Features of Not-for-Profit Organisations:

- Mission-Driven – The primary goal is to serve a specific cause rather than generate profits.

- No Profit Distribution – Any surplus revenue is reinvested into the organisation’s activities rather than being distributed to members or stakeholders.

- Legal Recognition – Most NPOs are registered under specific laws and may receive tax exemptions or other benefits.

- Funding Sources – NPOs rely on donations, grants, membership fees, and fundraising events to sustain their operations.

- Volunteer and Employee Structure – They may have a mix of paid employees and volunteers contributing to their activities.

Types of Not-for-Profit Organisations:

- Charitable Organisations – Focus on social welfare, such as helping the poor, sick, or underprivileged.

- Religious Organisations – Churches, mosques, temples, and other faith-based groups that promote religious activities.

- Educational Institutions – Schools, universities, and research organisations that provide educational services.

- Cultural and Arts Organisations – Museums, theatres, and cultural societies that promote arts and heritage.

- Environmental Groups – Organisations working on conservation, sustainability, and environmental protection.

- Healthcare and Medical NPOs – Hospitals, clinics, and medical research groups that provide healthcare services or research treatments.

Advantages of Not-for-Profit Organisations:

- Tax Exemptions: Many NPOs qualify for tax benefits, reducing their financial burden.

- Public Trust: People are more likely to support and donate to an organisation with a clear social mission.

- Community Impact: NPOs play a crucial role in addressing social and environmental issues.

- Grants and Funding: They may receive government grants, private donations, and corporate sponsorships.

Challenges Faced by Not-for-Profit Organisations:

- Limited Funding: Dependence on donations and grants can make financial sustainability difficult.

- Regulatory Compliance: They must follow specific legal and financial reporting requirements.

- Volunteer Management: Recruiting and retaining volunteers can be a challenge.

- Operational Costs: Despite being non-profit, they still have expenses like salaries, rent, and marketing.

Examples of Well-Known NPOs:

- Red Cross – Provides disaster relief and healthcare services worldwide.

- UNICEF – Focuses on child welfare, education, and healthcare.

- World Wildlife Fund (WWF) – Works towards wildlife conservation and environmental protection.

- Doctors Without Borders – Provides medical assistance in crisis situations.

Formation and Registration of NGOs (Non-Governmental Organisations)

Non-Governmental Organisations (NGOs) are established to serve a social, charitable, educational, environmental, or cultural purpose without seeking profits. The formation and registration of an NGO involve several legal and administrative steps, which may vary depending on the country. Below is a general guideline on how to form and register an NGO.

Step 1: Define the Mission and Objectives

Before registering an NGO, it is essential to clearly define:

- Mission Statement – The core purpose of the NGO.

- Objectives – Specific goals and activities the NGO will undertake.

- Target Beneficiaries – The community or cause the NGO will serve.

- Mode of Operation – How the NGO will implement its activities.

Step 2: Choose the Type of NGO Structure

Different countries allow NGOs to register under various legal structures. Common types include:

- Trust – Governed by a board of trustees and established under a Trust Act (in applicable countries).

- Society – A membership-based organisation, typically registered under a Societies Registration Act.

- Non-Profit Company – Registered under corporate laws (e.g., Section 8 Company in India, 501(c)(3) in the USA).

- Foundation – Focuses on funding and grants for social causes.

The choice depends on the legal framework and operational needs of the NGO.

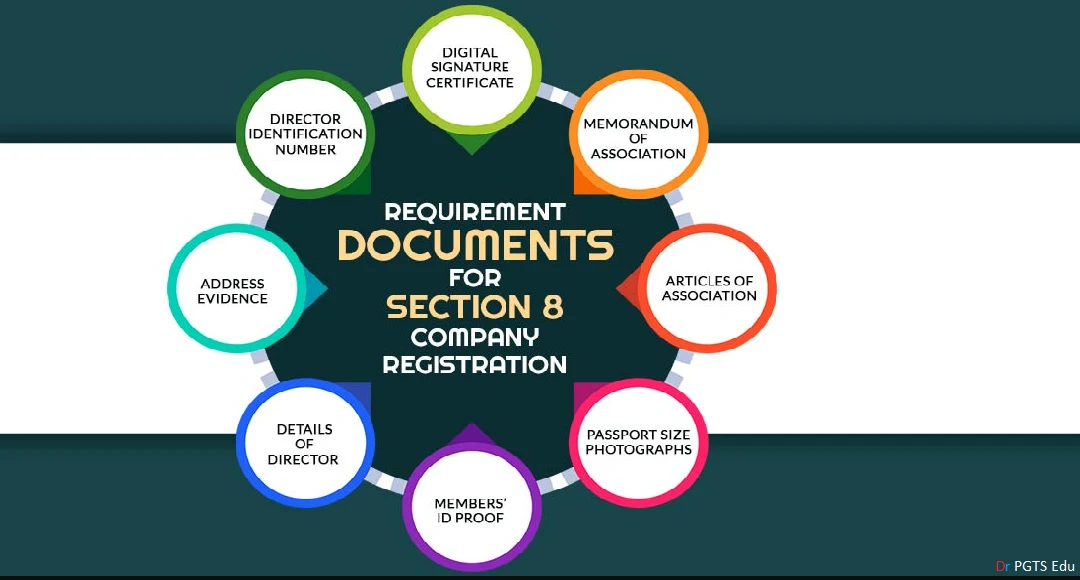

Step 3: Prepare Required Documents

To register an NGO, the following key documents are usually required:

1. Memorandum of Association (MoA) and Articles of Association (AoA)

These documents outline:

- The NGO’s name, location, and mission.

- Governance structure, including board members.

- Rules and regulations of the organisation.

2. Trust Deed (For Trusts)

For NGOs registered as a Trust, a Trust Deed must be prepared and signed by trustees.

3. Constitution/Bylaws (For Societies and Associations)

If registering as a Society or Non-Profit Company, a constitution or bylaws detailing the operational guidelines must be created.

4. Founding Members’ Details

- Names, addresses, and identity documents of the founding members.

- Minimum number of members required (varies by country).

5. Address Proof

Proof of the NGO’s registered office, such as a rental agreement or utility bill.

6. Board of Directors/Trustees List

A list of board members, their roles, and responsibilities.

Step 4: Register with the Relevant Authority

The NGO must be registered with the appropriate government body. Some common authorities include:

- Registrar of Societies (for societies and associations).

- Company Registration Office (for non-profit companies).

- Charity Commission (in some countries).

- Ministry of Social Welfare (for specific types of NGOs).

Registration Fee

A nominal fee may be required, depending on the country and type of registration.

Step 5: Obtain Tax Exemptions and Compliance

After registration, NGOs should apply for:

- Tax-Exempt Status – Allows the NGO to receive tax-free donations (e.g., 501(c)(3) in the USA, 80G in India).

- Donor Certification – Some countries require special certification to receive foreign donations (e.g., FCRA Registration in India).

- Annual Reporting – NGOs must maintain financial records and submit annual reports to the government.

Step 6: Open a Bank Account and Start Operations

- Open a dedicated NGO bank account for receiving funds and donations.

- Start fundraising and awareness campaigns.

- Hire staff or recruit volunteers.

Forming and registering an NGO requires careful planning, legal compliance, and proper documentation. Once established, NGOs can focus on fundraising, implementing programs, and making a meaningful impact in society.

Section 8 Company

Definition:

A Section 8 Company is a non-profit organisation registered under Section 8 of the Companies Act (India) or its equivalent in other countries. It is formed to promote charitable, social, educational, religious, or environmental objectives without distributing profits to its members.

Features of a Section 8 Company:

- Non-Profit Objective – The company operates for charitable or social purposes.

- Limited Liability – Members have limited liability, similar to other companies.

- No Dividend Distribution – Profits must be reinvested in the company’s objectives.

- Legal Entity – It enjoys a separate legal identity from its members.

- Governance – Managed by directors and governed by the Companies Act.

Exemptions Available to Section 8 Companies:

- Tax Benefits – Eligible for income tax exemptions under Section 12A and 80G of the Income Tax Act.

- No Minimum Capital Requirement – Unlike other companies, there is no mandatory capital requirement.

- Reduced Stamp Duty – Lower stamp duty is charged on registration.

- Relaxed Compliance – Some financial and audit compliance requirements are less strict.

Requirements for a Section 8 Company:

- Minimum 2 Directors (for a private company) or 3 Directors (for a public company).

- Minimum 2 Shareholders (for a private company) or 7 Shareholders (for a public company).

- A Registered Office Address within the country of incorporation.

- No Profit Distribution Clause must be included in the Articles of Association.

Application for Incorporation of Section 8 Company:

- Name Approval – Apply for name approval under the RUN (Reserve Unique Name) Service.

- Digital Signature Certificate (DSC) – Directors must obtain a DSC.

- Director Identification Number (DIN) – Each director must have a DIN.

- Application to the Registrar of Companies (ROC) – Submit documents like MoA, AoA, declaration, and financial projections.

- Approval and License Grant – Upon approval, the ROC issues a license and the company is incorporated.

- PAN & TAN Registration – Obtain PAN (Permanent Account Number) and TAN (Tax Deduction Account Number) for tax compliance.

Trust

Objectives of a Trust:

A Trust is formed to hold and manage assets for the benefit of individuals or the public. The objectives include:

- Charitable purposes (education, healthcare, poverty relief).

- Religious or spiritual purposes.

- Managing family wealth (in case of private trusts).

- Providing financial security for dependents.

Persons Who Can Create a Trust:

- Any individual with the legal capacity to contract.

- Companies or organisations.

- Government bodies (for public trusts).

Differences Between Public and Private Trusts:

| Feature | Public Trust | Private Trust |

|---|---|---|

| Beneficiaries | General public or a section of society | Specific individuals or families |

| Regulation | Governed by the Public Trust Act | Governed by Indian Trusts Act, 1882 |

| Tax Benefits | Eligible for tax exemptions | Limited or no tax exemptions |

| Purpose | Charitable, religious, or public welfare | Personal or family benefit |

Exemptions Available to Trusts:

- Income Tax Exemptions under Section 12A for registered charitable trusts.

- Donations to registered trusts can qualify for Section 80G deductions.

- Property tax exemptions may be available for charitable trusts.

Formation of a Trust:

- Define the Objective – Decide on the purpose of the trust.

- Choose Trustees – Select responsible individuals to manage the trust.

- Draft a Trust Deed – The legal document outlining the rules and operations of the trust.

- Register the Trust – Submit the trust deed to the Sub-Registrar of Assurances.

- Obtain PAN & Tax Exemptions – Apply for PAN and 12A/80G certification for tax benefits.

Trust Deed:

A trust deed is a legal document that defines:

- Name & objective of the trust.

- Details of trustees and beneficiaries.

- Powers and responsibilities of trustees.

- Rules for fund usage and asset management.

Society

Advantages of a Society:

- Democratic Structure – Managed by an elected governing body.

- No Minimum Capital Requirement – Can be started with minimal financial resources.

- Tax Benefits – Eligible for 12A and 80G tax exemptions.

- Easy to Expand – Can add new members without complex legal formalities.

- Greater Public Trust – Societies are often seen as credible for social causes.

Disadvantages of a Society:

- Complex Compliance Requirements – Needs periodic financial and activity reporting.

- Limited Operational Flexibility – Decision-making depends on the governing body.

- No Personal Benefit – Profits cannot be distributed among members.

- Risk of Internal Conflicts – Disagreements among members can hinder operations.

Formation of a Society:

- Minimum Members – Requires at least 7 members (India) or as per local laws.

- Draft a Memorandum of Association (MoA) & Rules & Regulations – Defines objectives, membership rules, governance structure.

- Registration with the Registrar of Societies – Submit documents to the local Registrar of Societies.

- Obtain PAN & Bank Account – Necessary for financial transactions and tax compliance.

- Apply for Tax Exemptions – To receive donation and tax benefits.

Tax Exemption for Societies:

- Section 12A – Grants income tax exemption for non-profit societies.

- Section 80G – Donations to registered societies qualify for tax deductions.

- GST Exemption – Some societies engaged in charitable activities may be exempt from GST.

- A Section 8 Company is ideal for structured governance and attracting donations.

- A Trust is best for long-term asset management and public welfare.

- A Society is suitable for member-based social or cultural organisations.

Read also: Setting up of business entities in india